Companies Simplified – Hindustan Unilever

-

By Parth Parikh

Have worked in the financial services industry for around 8 years now, and main areas of work have been Sector Research, Risk Management, Financial Modelling and Wealth Management.

Involved in the developoing content as a part of training in various Organizations like Kotak Securities, Motilal Oswal, Nippon Mutual Fund(erstwhile Reliance Mutual Fund), JPMC, Crisil.

HUL Company Analysis is an interesting one if you are studying India’s FMCG Sector. India’s USD 70 Bn FMCG market is the major contributor to India’s GDP. The household and personal care segment is the primary driver and accounts for 50% of India’s FMCG sales.

With 50+ brands across 15 distinct categories, HUL dominates the FMCG market in India. 90% of households in India use one or more HUL brands. It has also entered the top 15 global consumer staple stocks list with a current market cap of USD 75Bn. So, let us see some interesting facts in this HUL company analysis.

- Reach in 9 million+ outlets in India (i.e., 60% of India’s outlets).

- One of the largest distribution networks in India with 3,500+ distributors.

- #1 in 8 product categories (Skincare, skin cleansing, hair care, fabric wash, household care, tea, health drinks, ketchup).

- Leading fabric wash brand (surf excel) generates Rs. 5,000+ Cr. revenue. And with a market share of ~18%, it accounts for 14% of its revenue and 45% of its laundry segment sales.

- Two brands generate Rs. 5000+ Cr. Revenue.

- Seven brands generate Rs. 2,000+ Cr. Revenue.

- Sixteen brands generate Rs. 1,000+ Cr. Revenue.

With that, let’s see how does HUL position itself as a brand

HUL markets itself as a multi-local multinational. It is the Indian subsidiary of Unilever PLC that holds ~62% of the share in the company and offers international expertise to the service of local consumers in the broad spectrum of product categories defined in its mission statement.

![]()

HUL offers its products according to the taste and preference of the local consumers as India is not a homogeneous market. It includes customers from various clusters based on their socio-economic attributes and it provides value to customers in terms of price and quality.

It has a robust competitive performance, with ~85% of its business is gaining penetration and >90% of business is winning a share of the market. Hence, Forbes ranked HUL as the most innovative company in India and 8th globally.

With this, it’s critical to understand HUL segments & revenues

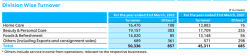

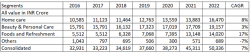

HUL has classified its business into four broad divisions. Given below is the division wise revenue contribution.

- Home care ~32%

- Beauty & personal care (BPC) ~38%

- Food and refreshment ~28%

- Others ~2%

Total revenue for HUL in FY 2022 was Rs. 51,193 with YoY growth of ~11%. The BPC segment is discretionary, and its demand is more affected by macro-economic factors; still, it continues to be a significant driver and generates ~38% of revenue for the company.

HUL continues to strengthen its market position in the BPC segment by driving penetration in core brands, such as Dove, Ponds, Sunsilk, and dominate the hair care and skincare category market.

Registration Open - Analyst Program Click here

And what about division-specific growth?

The Home Care segment grew 19% in 2022, led by double-digit growth in both Fabric Care and Household Care. Stable growth has been experienced by the BPC segment.

The foods and refreshment segment has shown a significant growth because of its acquisition of GlaxoSmithKline Consumer Healthcare (GSKCH) in 2020.

Growth in other segments, including infant and feminine care is declining.

Now the question is, how has the merger improved the growth prospects for HUL?

HUL acquired GSKCH for Rs.40242 crores. HUL leveraged its distribution network and distribute GSKCH brands in India.

This primarily expanded the nutrition and health drinks business which remains underpenetrated in India as Horlicks is a #1 brand in the health and food drinks segment and have a volume share of 50%.

HUL introduced new pouch packs and Rs.2 sachets for Horlicks and Boost to drive trials and unlock newer market. Company has also expanded Boost across India.

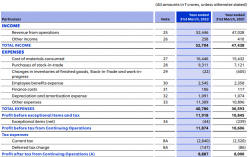

Moving on to profitability now…

HUL operates at a gross margin of ~70%, an operating margin of ~24%, and a net margin of 17%.

The beauty and personal care segment is the major contributor and accounts for 1/2 of the profitability for HUL.

FMCG business operates on reasonably low margins, as you can see that net margins for HUL over the last seven years is in the range of 12-17%. But the efficiency of the business depends on churn rate and inventory management.

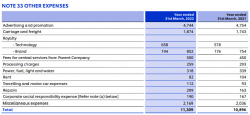

The interesting thing to note over here is, they spend just over 9% on Advertising and Promotions.

Registration Open - Analyst Program Click here

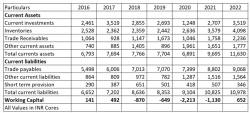

So, how does HUL manage the working capital cycle?

Companies in the FMCG sector generally operates with a negative working capital because of efficient supply chain management. The industry has low debt and usually financed by creditors.

If you see HUL, then over the last few years, it operates with negative working capital. Let us see some ratios for FY 2022 and understand its working capital cycle.

So turnover ratios suggest how efficient a company is to manage its working capital, including inventory, debtors, and creditors.

HUL has a negative working capital cycle of 20 days. That means the company receives inventory on day one and sells it on day 30th. It accepts cash on day 46th (30+16). And no money leaves the company until day 66th when the suppliers are paid. This is beneficial for the business as money is not going out, and it provides funding to the company for 20 days.

Thus, because of its brand loyalty, HUL can sell products and generate cash quickly before it has to pay the bills to its suppliers.

What’s in it for the shareholders?

HUL has a low capital intensity and has a marketing expense of ~9% of the revenue. It does not engage in a direct price war with its competitors; instead, try to outspend on marketing and advertisements. This creates a healthy, profitable scenario in the industry. And HUL profits have grown 2.5x over the last ten years. And the stock price almost 8 times 🙂%

This has generated stellar returns for its stakeholders, where:

ROCE is consistent 100%+

Please note ROCE and ROE are taken from annual reports and Return on Net Worth and Return on Capital Employed have dropped from financial year 2020-21 on account of an increase in shareholders’ equity pursuant to the merger of GSK CH.

So HUL offers almost everything, whatever is expected from a perfect business. With its diverse product portfolio and robust distribution network, it has created a wider reach even in the interiors of the country and has positioned itself as a brand.

Other Trending Posts in this Series – DMart Valuation | PVR Cinema | Urban Company

To stay updated about all of our posts on Businesses and Finance Careers – register and create a free account on our website. You will also get access to a free Finance Bootcamp course once you register.

-

About the Author

Have worked in the financial services industry for around 8 years now, and main areas of work have been Sector Research, Risk Management, Financial Modelling and Wealth Management.

Involved in the developoing content as a part of training in various Organizations like Kotak Securities, Motilal Oswal, Nippon Mutual Fund(erstwhile Reliance Mutual Fund), JPMC, Crisil. -

-

Register and get regular updates of new Blogs and access to Free Courses

-